Porsche: Biggest IPO of 2022

Oct 04, 2022Volkswagen finally spun out its most profitable brand: Porsche. Porsche IPO'd last Thursday on German exchanges and...wow.

It was kind of a dud.

Shares popped to 86€ before settling right near their IPO price at a comfortable ~82€ a share. This still makes Porsche nearly a 75 Billion market cap company--but usually the market sees an IPO with so little movement as pretty lame.

That's the thing though, we really like lame IPOs here at Moby.co. SPAC fever back in 2021 created some truly brain-breaking valuations for literally anyone with half a business and enough capital to afford the fees to get listed. It's nice seeing a middle-of-the-road, boring IPO for what is actually a pretty solid business.

But with any IPO, there is going to be a little volatility in the first few weeks. While we like Porsche’s current valuation, we want to offer a few other options in case the market catches a little buy-fever.

Let’s look at how to play this👇

Porsche Overview:

We don’t need to explain Porsche, right? One of the most timeless luxury performance car brands of all time—Porsche has long been a part of the Volkswagen auto empire.

We talk about Tesla and other American car manufacturers so much that it’s hard to remember that VW is the biggest carmaker in the world—with Porsche being the most profitable member of that conglomerate.

Spinning Porsche makes a lot of sense for VW -- especially with how much control they are retaining.

They get capital from the shares they still control, and their valuation gets favorably compared to Porsche’s slightly spicy P/E ratio. VW hoped to raise €9 Billion with this IPO by listing 25% of Porsche's preferred shares on the market. VW and parent company Porsche SE are retaining the majority of the remaining shares.

VW is going to use that capital to charge up their push into the EV space—hoping to rival Tesla’s EV production by 2025 (or 2024 if you’re buying into the VW hopium a little too hard).

Furthermore, the spin makes sense for Porshe because they can finally attain those slick luxury car valuations the market loves so much.

Porsche Valuation:

On the surface—Porshe’s initial valuation may look pretty wild as it’s valued almost as much as the company it spun out from. But this makes sense when you look at how the market values high-margin plays like Ferrari and Tesla.

And that lens is what makes Porsche an attractive buy right now. Let’s do a quick deep dive into Porshe’s margins:

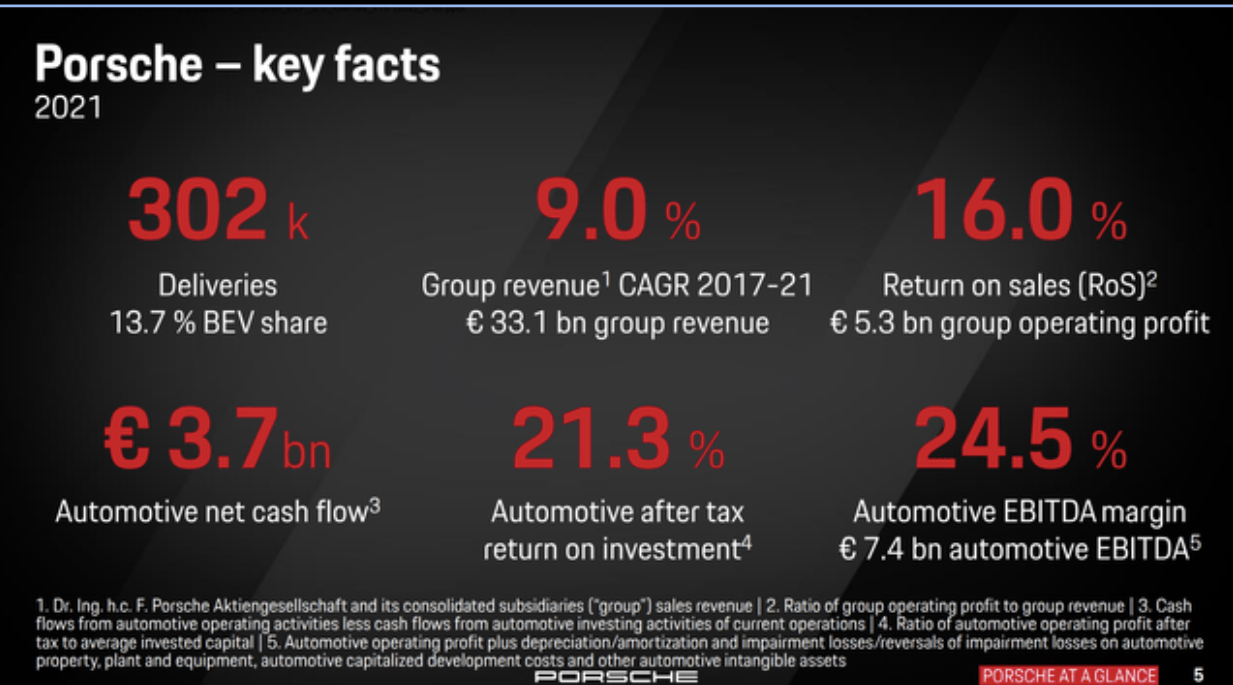

Porsche is a lower-volume, high-ticket carmaker. With margins in the 20% range—that puts them in Tesla’s neighborhood (when looking at cars only) but WAY behind Ferrari’s truly incredible ~50% net margins.

So that could be seen as a good reason to not buy the stock until we check how the market is currently valuing these companies. Right now Ferrari is trading at about 40x earnings, while Porsche is just shy of 18x (at the time of writing).

For us, that’s a clear sign that Porsche’s IPO is being potentially slightly undervalued thanks to how wild the market is currently.

This is a stock with room to run—and Porsche’s valuation makes them a nice “bridge” company between the wildly expensive Ferrari and Tesla stocks and traditional automakers with P/E ratios in the single digits.

Porsche Growth:

But if Porsche is such a margins powerhouse—why is it being valued so low compared to Ferrari? It's not just an issue of margins—it's an issue of growth.

Porsche's profit grew 12% in the first half of 2022 compared to H1 2021. Ferrari's margin growth edged out Porsche at 13%. But that tiny sliver in margins isn't enough for such a huge gap in how much the market is valuing these two stocks.

The key appears to be pure revenue growth. Ferrari is going to stay as our example—who has been able to grow revenue 20% in H1 2022 compared to H1 2021. Porsche—much larger and potentially much closer to market saturation—was only able to grow 8% in the same time period.

For us, that's the key differentiator. Porsche is going to potentially keep growing slowly in 2022 with rising costs and an ongoing inflation crisis battering European countries. Porsche certainly has margins to eat into, but their margins are the thing that primarily makes the stock value.

It's harder to compare Porsche to Tesla's growth because Tesla has been playing with EV margins for its entire existence. Furthermore, Porsche is more legacy than Tesla still and therefore more prone to grow slowly. That's why we're mainly focusing on Ferrari as our basis for comparison.

This slow growth is absolutely the main factor holding Porsche back.

Porsche can very much overcome this as the economy churns through this weird period of busted supply chains and inflation. Luxury brands don't really feel the pain of inflation, but more potentially "attractive" options on the market like Ferrari and Tesla may keep folks from buying.

However, that entire thesis gets thrown out the window in a world where Porsche doubles down on EVs. EVs bring simplicity that offsets how expensive their materials are, and bring a lot of new buyers who otherwise would have gone with Tesla.

Porsche Outlook:

While that valuation seems good, Porshe’s long-term outlook really hinges on their EV push.

Their Taycan EV model has been really successful, and they have 3 other models they are actively developing. If Porsche can hit their goal of 50% electric sales by 2025, it can easily grow into this valuation and take off.

If they get stuck with a majority of complex combustion vehicles -- they’ll likely miss out on the margins that their 18x revenue valuation is currently counting on.

So if you're buying into this IPO, you need to be a believer that Porsche can hit these goals (or at least come close). For us right now, it's a bit early to confidently say wheter or not they can -- however they've shown to be making serious strides in the right direction.

In any case, Porsche is maintaining a close relationship with VW—who is putting truly serious money behind their EV initiatives.

We are therefore confident that this IPO is a huge step towards giving Porsche and VW the capital they need to fight for limited Lithium and Nickle resources as EV competition begins to seriously heat up in the next three years.

So growth honestly looks decent enough for us to be long-term speculative buyers, but the final factor to consider is that most of our audience is in the US, and buying Porsche stock comes with a lot of fees until they make a listing on a US exchange.

Porsche's growth trajectory looks like it can just barely edge out any inefficiencies that come from the hassle and fees that come from buying foreign stocks (depending on what brokerage you use). It absolutely can pull that off if they pull off an EV breakout, but that's really hard to predict as competition heats up.

However, if you want something a little less spicy given the fees you might have to pay to buy Porsche stock—this IPO will ultimately produce positive results for VW as well, so consider a buy there instead.

Regardless, we love watching new players emerge for the coming EV race of the mid 20's. It’s gonna be a wild ride, y’all