Titan Medical: A Strong Penny Stock Over The VERY Long Term

May 04, 2021🔑 Key Takeaways

A potentially disruptive new player in the surgical robotics market.

- Titan Medical has a potentially best-in-class single-port robotic surgery device that is expected to go to market in late 2022 or early 2023

- Titan Medical’s Enos surgical robot hopes to break away from its competitors by being easy-to-learn for surgeons, portable and low-cost while still offering best-in-class flexibility and functionality for the subspecialties it serves

- This device could lead a potentially $6 billion market currently dominated by Intuitive’s da Vinci SP, a device its many competitors believe has fallen behind and leaves a large amount of unmet need

- Several other robotic surgery companies serving subspecialties have been acquired for over $1B by major players in the medical device space. Titan Medical already has a multi-million dollar partnership with Medtronic that could lead to an acquisition

🔎 Stock Profile

Getting to know Titan Medical:

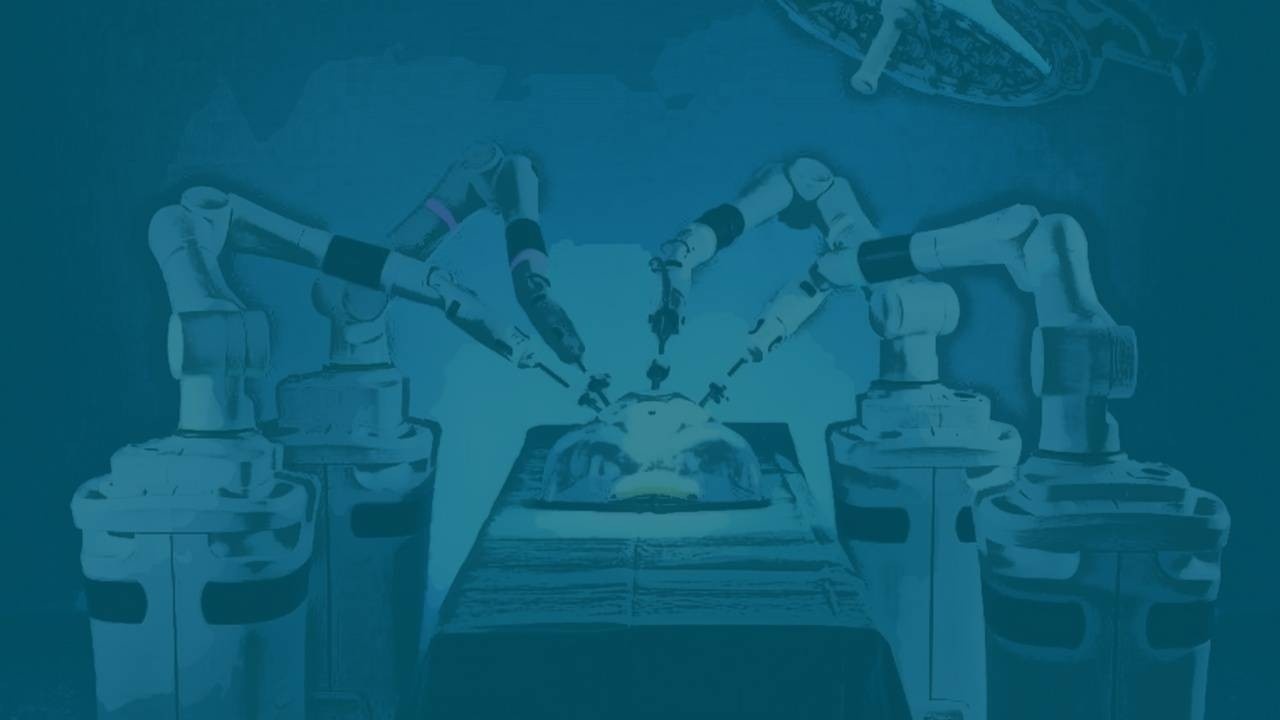

Titan Medical’s primary claim to fame is their Enos Single-Port Robotic Surgery System. Its advantage in the market is that it is an easy-to-learn, portable and low-cost surgical robotics system that offers a high degree of flexibility and functionality while reducing operator fatigue. They’ve worked with countless surgeons, many of whom are world class names and some of whom serve directly on their advisory board, to create and refine a system that’s comfortable for surgeons to use and reduces patient trauma and scarring. The system is also more mobile and easy to use than most of what’s on the market, allowing the system to be easily moved between ORs and picked up within hours by veteran surgeons. Although their initial pursued indication will be benign gynecologic surgeries they aim to have their Enos system used in colorectal, urological, other gynecological and general abdominal surgeries as well.

The Enos has already been used in 45 procedures across the world, primarily in the gynecological, urological and colorectal fields. Some successful uses in procedures have been tested by eager surgeons that the Titan Medical team hadn’t even originally intended for the system. A surgeon has never failed to succeed using Titan’s system thus far, even when using it for the first time. Most surgeons using the system have gotten the hang of using it within an hour with Titan’s VR Training modules.

The full Enos kit consists of 3 key components.

- A Surgeon Workstation that contains a 3D HD display mounted to an ergonomic workstation with a handle interface that’s designed to be comfortable for a surgeon to sit in for hours on end, a key problem in the operating room that surgical robots are looking to solve. The workstation is small and mobile so it can easily be moved from OR to OR with ease, a feature that is not common in current robotic surgical systems and helps reduce hospital costs.

- The Patient Cart contains the instruments, the cameras and everything the surgeons are going to use to cut. It contains a 25mm insertion tube that contains the two multi-articulating surgical arms and two lighted HD cameras that will all enter the body through a single-port incision. The system will be able to elevate, tilt and pan to retain visibility under surgeon control at all times and will also have instruments that will be easy to load and replace. Just like the workstation, the cart is highly mobile and contains minimal cabling so it can be easily maneuvered from OR to OR.

- Titan’s Multi-Articulated Instruments, which are located in the patient cart, will be the tools used for the surgery. These two arms, which look like miniature Doctor Octopus arms, are extremely fluid and flexible, yet strong so they can grasp, suture, and coagulate with ease. These arms currently have 8 different tip types for various different uses but are designed with an open architecture system that will easily allow Titan to develop new functionality and tip types to adapt to potential future needs.

Single Port vs Multi Port and What You Need to Know About Surgical Robotics

Something that I mentioned a few times so far is the term Single port. This is a key area in which Titan is attempting to set itself apart from its competitors. I’ll explain a bit more here the differences between single-port and multi-port surgical robots and the robotic surgery field as a whole.

As mentioned, there are 3 types of surgery options to consider when it comes to comparing surgical robots - single port, multi-port surgery and old-fashioned surgery. Titan’s Enos, Memic’s Hominis and da Vinci’s SP are single port options and CMR’s Versius, J&J’s Ottava, Medtronic’s Hugo and Transenterix’s Senhance are multi-port options.

Old-fashioned surgery is exactly what it sounds like and likely what you’re used to when you think of surgery. Surgeons often need to make large incisions to give them plenty of room to work with that cause a fair amount of trauma and require lots of stitches. Cosmetically, it usually looks pretty unappealing as well.

Robots are the future because they offer more precision, can let the doctors sit instead of standing up and leaning over for hours-long surgeries and allow much less scarring (even the lower quality multi-ports reduce surgical damage by 75%). These surgical robots are divided into single-port and multi-port.

Multi-port basically means it requires multiple incisions vs a single port’s single, often smaller, incision. Aesthetically, patients tend to prefer a single port incision since the less scars the better. Sometimes single port abdominal surgeries can even go straight through the belly button, the vagina or other natural orifices, leaving no scarring at all. Single port surgeries can also offer better mobility and room to work for the surgeon vs multi-ports where the surgeon’s operating area is sometimes constrained.

Single-port surgeries are not always possible as they require a somewhat large internal field to operate in. They’re often best for more common, simpler procedures but they do them very well. There’s a market for both, but where possible and safest to do so, single-port is likely to be the preference.

The Competition:

Competition in the field of surgical robotics is heavy. Intuitive is the current market leader but their current slate of robotic surgical systems is leaving competitors with plenty of room to innovate in a rapidly growing market worth billions.

Intuitive’s da Vinci SP, Titan’s most direct competition from Intuitive’s surgical suite and the current market leader, is a single port robotic surgery system as well. However, their system is expensive, it’s very large, it’s unwieldy and it has limited use in the types of procedures it can perform, with many simple minimally invasive procedures that the Enos aims to cover being out of the da Vinci SP’s wheelhouse. In the surgical areas of overlap between the two systems (which mostly seem to be urological), Titan’s Enos has a very good chance at becoming the preferred device to the da Vinci SP. For Intuitive to retain its advantage against Titan Medical and many other competitors, they’ll need to innovate on their current system.

CMR Surgical’s Versius, J&J’s Ottava, Medtronic’s Hugo and Asensus’ (formerly Transenterix) Senhance are all multi-port systems attempting to serve general surgical needs and intending to compete with Intuitive’s da Vinci. However, despite being multi-port systems, they could still take up valuable market share away from Titan’s Enos. Of the 4, CMR’s Versius seems the most likely to compete more directly with Titan’s Enos, despite being a multi-port system. The Versius, like the Enos, is cheaper, smaller, more portable and easier-to-use than the da Vinci. The Versius is also currently under FDA review and if approved, will be on sale to the general public before the Enos. Titan’s main advantage is that it is single-port and has some design advantages in some of the Enos’ areas of specialization.

J&J’s Ottava is intended to give a greater range of flexibility and control and take up less space while also being easy to use. However, it may not be nearly as portable as the Enos, the Versius or the Hugo (if at all) and is years away from FDA approval, with clinical trials not set to begin until 2022. Asensus and their Senhance system is plagued with enough controversy that the company, formerly known as Transenterix, felt they needed to change their name. While the Asensus is the only system on this list besides the da Vinci approved to market for multiple surgical areas, the system itself has few advantages over the da Vinci and, in its early days before much-needed improvements were made, struggled with adoption due to surgeons just flat out not liking using the system. During these struggles, Asensus took investors for a ride, diluting shares repeatedly and using desperately needed R&D funds on marketing and payouts for company directors.

Medtronic’s Hugo, which has an IDE filed and aims to be on the market this year, is portable yet larger than the Enos or Versius. Titan Medical however, doesn’t see the Hugo as a competitor. Although I’ll be covering this in greater detail later, Medtronic is invested in Titan Medical and has a development deal that involves using Titan’s patents and development of technologies that could be used in the Hugo or some of other Medtronic’s other systems. Medtronic’s collaboration and investment in Titan Medical means they likely see some value in Titan’s alternative approach, while CEO David McNally has previously addressed these differing approaches as allowing the two companies to have a synergistic relationship in the pursuit of success with their respective surgical robots.

Finally, one of the last and most notable competitors is Memic’s Hominis. Like Titan, they have a single-port system that is advertised as cheaper and one that takes up less space in the operating room. Their initial indication is, like Titan Medical, to be used in benign gynecological surgeries and they are aiming to get approvals for ENT, Thoracic, Urologic and Gastrointestinal uses. The biggest advantage they have over Titan Medical is that they have recently been FDA-approved, a milestone that Titan Medical won’t be on track to replicate for at least another year.

However, Titan Medical seems to have the advantage in technology. The Enos workstation is superior to the Hominis, which has a smaller display and no room to sit to relieve operator fatigue. The Enos also seems to be potentially more adaptable with its multi-articulated instruments and more portable than the Hominis. David McNally was asked to directly address the Hominis’ approval in a recent Investor Conference and he stated that he firmly believed the Enos will prove its superiority to its potential competitors.

A Potential Acquisition

The robotics surgery market is ripe with acquisitions and Titan meets many of the same requirements as others who have been previously acquired. Mazor Robotics is a robotic spine surgery device that was eventually acquired by Medtronic for $1.7B in 2018. Medtronic has invested $10M in Titan and looks very well-positioned to do the same should FDA approval and other requirements be met.

Johnson & Johnson recently went on an acquisition spree in the robotic surgery market. They acquired Verb’s prototypes of a fully-automated surgery system and Auris Health’s robotic lung biopsy system, the two of which are now merging into their previously mentioned multi-port Ottava general surgery system. They also acquired Orthotaxy’s orthopaedic system. Auris’ acquisition alone was worth $3.4B in 2019.

Based on the pricing of other acquisitions in this field, an acquisition of Titan by Medtronics may likely be worth over $1B, just a little over 7x Titan’s current market cap as of this writing.

Management

Titan has an outstanding leadership team consisting of many industry vets, many of whom have led their own successful medical device companies.

CEO David McNally has an outstanding track record with medical device companies, having led several successful companies while generating immense shareholder value during his tenure. He has 33 years of experience in the medical device industry and is even listed as a co-inventor on 40+ patents.

Titan’s current head of research, Dr. Perry Genova, has led 4 different medical device startup companies of his own, some of which were acquired. The rest of the leadership team consists of individuals who are veterans in their respective fields, with not a single member with anything less than 15 years of industry experience.

Their surgical advisory board is full of world-renowned surgeons, many of whom could be considered leaders and innovators in the field of robotic surgery. They have the current Vice President of the American Association of Gynecologic Laparoscopy, a board member of the Society of Robotic Surgery, the editor of ‘Surgical Innovation’ and the former Director & President of the American Board of Colon and Rectal Surgery.

Some of these members have written hundreds of papers and articles on robotic surgery and others have single-handedly trained thousands of surgeons and performed thousands of surgeries, often being requested to travel all over the world to do so. The surgical advisory board has been and continues to be heavily consulted on the design for the Enos surgical robotics system.

Financials

Titan Medical’s financial situation has improved drastically in the past year. As of January 31, 2021, the company had $42.5 million in cash on hand and secured an additional $23 million in a bought offering in February. Their historical cash burn puts them at roughly $2 million per month and the company expects the current cash on hand to fund operations through at least most of 2022 and potentially the public launch of the Enos system. Titan is also on track to receive an additional $21 million from hitting certain additional milestones related to their deal with Medtronic, which would further strengthen their cash position. This is quite healthy for a pre-market biotech and makes additional offerings and dilution less likely in the near future. To be noted however is that their first and only current source of revenue is this licensing deal with Medtronic.

Risks

Besides the typical pre-market biotech company risks, like the potential for their flagship product to not receive regulatory approval, Titan Medical has 2 key areas of risk: time and competition, both of which are somewhat intertwined.

The competition aspect is somewhat apparent in what I’ve already written. This market is currently underserved but many companies are trying to take advantage of that. Titan Medical needs to directly surpass the Hominis and the da Vinci SP, which have the advantage of being able to establish themselves in the market ahead of Titan Medical. The Hominis specifically is already serving the exact subspecialty Titan Medical is aiming for. The Enos currently seems to be the technologically superior option to these systems in key areas, but these advantages will need to be attractive enough to leap above what will be somewhat entrenched competitors.

Many of Titan Medical’s multi-port competitors look closer to fundamental parity than its single port brethren. Natural orifice and single port incision surgeries will need to remain popular enough that Titan Medical has room to carve its own niche. In this aspect at least, Titan Medical seems to have an advantage as current at-market multi-port competitors with advantages over da Vinci’s single-port platform have struggled, which suggests that the appetite for single-port surgeries is high.

And, as mentioned, time. Titan is still potentially 18-24 months from going to market. In this time, a majority of their multi-port competitors will have made it to market, the Hominis will have been on the market for at least 18 months and Intuitive themselves will have time to adapt and improve the da vinci to better address competitors. This is the single biggest risk factor for Titan as they will have little first mover advantage and will be relying completely on the merits of their tech and marketing/sales team in order to gain a foothold in the market. That being said, some of the main issues with Intuitive’s da Vinci SP will be difficult to address without bringing an entirely new device to market, which would put Titan in the lead.

Final Thoughts

Titan Medical is a potentially leading competitor in a crowded field, but even should it fail to dominate that lead, Titan Medical has plenty of opportunity to succeed and rise exponentially above its current value. Successfully going to market and taking even a portion of what’s available should see their value double or triple at minimum.

Including the cost of servicing the robots and future upgrades, the robotics surgery market is estimated to have a potential future value of $18 billion by 2025. The abdominal surgery market alone (Titan’s target market) is estimated to be worth $6 billion by 2023. Titan’s initial benign gynecological indication, with which they’d only be competing with the Hominis initially, is estimated to be worth $1 billion based on Titan’s internal revenue estimate

When Transenterix had its initial run after FDA approval for abdominal surgeries, it temporarily reached a market cap of $1.2 billion. Other surgical robotics device companies with limited subspecialties were acquired for $1.7 billion (Mazor) and $3.4 billion (Auris), something that Titan Medical is well-positioned for due to their current relationship with Medtronic, which is similar to the one Medtronic had with Mazor before their acquisition.

Taking into account the total addressable market of their product and what I’ve mentioned above, I rate Titan Medical as a speculative BUY and set a 2023 price target of $10, with room to grow. Should Titan Medical become the target of an acquisition or gain FDA approval somewhat ahead of schedule in 2022, I expect this price target to be reached before then.

If you choose to jump in now, expect lots of volatility In the short term, with a price mostly dictated by trends in growth stocks, small caps and biotechs in general as material news on their flagship product is not expected in the near term.